Date: 5/24/2022

Author: Mr. X

When it happened about two months ago, it was heralded as a sign of the apocalypse. “The yield curve inverted,” was muttered with dark purpose, as if a prophecy was being confirmed. The way people spoke about it was as if it was a part of a horror story. It reminded me of The King In Yellow, where those who read a forbidden book end up going mad.

Unfortunately for us, markets aren’t just about numbers. They are about human beings and their emotions. Collective madness has consequences.

It’s true, an inverted yield curve may indicate recession. However, it doesn’t necessarily follow. Even if a recession hits, it doesn’t follow a fixed schedule.

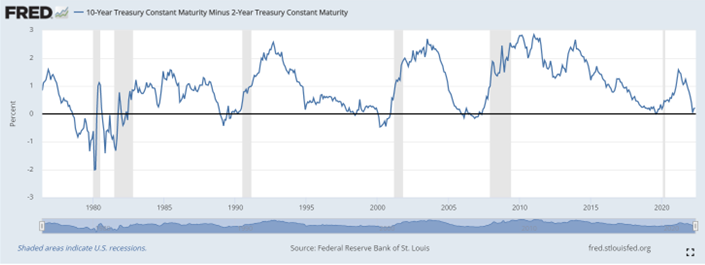

The yield curve plots the interest rates of bonds that have equal credit, but different maturities (the time until they can be redeemed). Normally, the interest you get for a bond with a longer maturity (like a 10-year Treasury bond) would be longer than the interest you get for a shorter bond (like a 2-year bond). This makes sense, because investing in a long-term bond is a bet that the issuer will be stable enough to pay it off even in a semi-distant future. Predicting the short-term is easier so you don’t get as much interest.

This is simple and logical. Now think about what it says about the government and society if short-term U.S. Treasury bonds carry higher rates than long-term U.S. Treasury bonds. It’s a sign people think that the short-term is going to be exceptionally volatile. It’s an expectation of trouble. It is a revealed preference that shows people fear recession.

It’s our Yellow Sign.

You can use different spreads to look for an inverted yield curve, such as the 10-year bond and the 3-month bond as opposed to the 10-year bond and the 2-year bond. For our purposes, we’ll use the 10-year bond and the 2-year bond, which is the most commonly used.

This curve inverted on April 1 of this year.

Since 1956, an inverted yield curve has preceded every recession. Bespoke, in research that was widely circulated in the press when the curve inverted, said “there has been a better than two-thirds chance of a recession at some point in the next year and a greater than 98% chance of a recession at some point in the next two years.”

In data provided by the St. Louis Federal Reserve, you can see that recessions (indicated by the shaded areas) follow after the curve inverts.

However, the time between the inversion and the recession can vary. It can be anywhere from 6-18 months, which doesn’t provide much practical guidance about what you should do right now. If you constantly predict a recession, eventually you will be right. If you can’t say when it will happen, your prediction is worthless. Advisors Capital Management partner and portfolio manager JoAnne Feeney said basing predictions on the yield curve is “dangerous” because it might detract from more positive and important data about job growth and reopening.

According to data from Statista Research Service, “Over the last five decades, 20 months, on average, has elapsed between the initial yield curve inversion and the beginning of a recession.”

MUFG Securities, quoted in CNBC, reported: [T]he yield curve inverted 422 days ahead of the 2001 recession, 571 days ahead of the 2007-to-2009 recession and 163 days before the 2020 recession.

Foreign Energy Expert Predicted “Big Oil’s” Recent Surge

With the 7 triple-digit wins under his belt in 3 months, he’s now showcasing the technology he used to do it.

Click the link here to get the full details.

BCA Research, quoted in Barron’s, “found that the gap between 2- and 10-year yields has inverted before seven of the past eight recessions, with no false signals.” Using the spread between 3-months and 10-year yields is even more accurate, predicting all of the past eight recessions.

The Fed itself dismissed the importance of the “2-10 spread” in a March 25, 2022 note (about a week before the curve inverted). The authors said “the perceived omniscience of the 2-10 spread that pervades market commentary is probably spurious.” They argued this measure had no power in and of itself.

Ultimately, we argue there is no need to fear the 2-10 spread, or any other spread measure for that matter. At best, the predictive power of term spreads is a case of “reverse causality.” That is, term spreads predict recessions because they impound pessimistic—often accurately pessimistic—expectations that market participants have already formed about the economy, and thus an expected cessation in monetary policy tightening. Thus, term spreads could have little or no economic impact in and of themselves. Nevertheless, as FDR might have pointed out, it can only make things worse if investors not only fear the prospect of a recession, but at the same time, are spooked by that fear itself, which is mirrored in inverted term spreads.

However, you can probably understand why the Fed would want people to make no connections between inverted yield curves and recession. The central bank wants to show it has control and can perform a “soft landing” for the economy. If people fear there will be a recession instead, it could be a self-fulfilling prophecy.

Of course, that cuts to the heart of it. Dismissing yield curves as spurious or coincidental denies the psychological essence of markets. Something is worth what people think it is worth. If an inverted yield curve really did do nothing but measure “fear,” there is still value in that.

There’s reason to think there’s more to it than that. The Federal Reserve Bank of San Francisco published economic research in 2018 that backed the yield curve’s predictive power. Using the 1-year note versus the 10-year note between January 1955 and February 2018, it found:

Every recession over this period was preceded by an inversion of the yield curve, that is, an episode with a negative term spread. A simple rule of thumb that predicts a recession within two years when the term spread is negative has correctly signaled all nine recessions since 1955 and had only one false positive, in the mid-1960s, when an inversion was followed by an economic slowdown but not an official recession. The delay between the term spread turning negative and the beginning of a recession has ranged between 6 and 24 months.

Still, one could argue that this measure is less valuable now than it was in the past because the Fed has interest rates so low. That could arguably make it easier for the curve to invert.

We can also think of an easy example of correlation, not causation. In 2019, the curve briefly inverted. The economy did indeed dramatically contract soon afterward, but that was entirely due to COVID-19, not some failure in monetary policy.

Thus, one might simply shrug this sign off. NBC reported even after the yield curve inverted that “many economists believe a formal recession – the economy going into reverse for two consecutive quarters – is not imminent.”

In these extraordinary circumstances, one might even say that a briefly inverted yield curve is a good thing. The yield curve inverted at a time when the Federal Reserve was trying to convince the markets it could stop inflation. Ashwin Alankar argued that the inverted yield curve was a sign investors believed in the Fed’s approach to fighting inflation.

[I]f the market thought the Fed had truly lost its way, we’d now be witnessing a steepening—not a flattening—yield curve. The fact that yield increases on Treasuries with maturities of 5 years and longer have not kept pace with the 2-year, in our view, means that the market sees the Fed’s approach to controlling inflation as credible.

The problem with this approach is that even the Fed admits there are uncontrolled factors that could tip us into a recession. Rising food, fertilizer, and energy prices will create inflationary pressures that can’t simply be dampened by raising interest rates. Diesel costs alone are up 75% over the last year and that is going to have an impact on everything else. Concerns over food supplies are so great the Indian government has banned wheat exports, infuriating its own farmers. Over all of this is the prospect of a war that I don’t see ending anytime soon, probably not even this year (barring regime change in Moscow.)

Even if it is simply a measure of fear, rather than an objective technical signal that recession is imminent, it’s worth paying attention to the inverted yield curve. It doesn’t necessarily mean that America is headed into a recession, but it would be the first time it’s been wrong in decades.

More importantly, for America to avoid a recession requires the Fed to get everything right – and for the world to avoid complicating the situation further. With tensions rising in Iran, Israel, Taiwan, and all of Europe, that’s not something we can count on. An inverted yield curve isn’t an automatic confirmation of doom – but it’s the Yellow Sign warning us to slow down, be cautious, and remember that if enough investors are overcome with fear of a recession, they’ll end up manifesting it.

Mr. X is an investment analyst working in the Washington DC area who specializes in the intersection of business and public policy. After fifteen years working in politics, he writes on a classified basis for RogueInvesting.com to bring you news on what those with power are debating, planning, and doing.