Date: 3/29/2021

Date: 3/29/2021

Author: Kent Moors, Ph.D.

If there is one factor today overshadowing everything else confronting investors it is the concern over inflation. Most would conclude that there is nothing more likely to tank a bull run than rising prices.

Well, not so fast.

There is bound to be an uptick in inflationary pressures at some point. Especially these days, following upon the worst market collapse since the Great Depression. We still have the effects of the coronavirus pandemic affecting investments, but the economy is clearly on the rebound with all indices now higher than they were before the coronavirus-induced closures and crash. And a recovering economy, especially one rising from the depths of what COVID caused, is going to experience some increase in prices. Hardly a bad thing in itself.

What bothers some insiders is the impact this is likely to have on the carry trade. For some time, especially after the Fed stepped in to put a heavy ceiling on interest rates, a largely artificial way of making money intensified.

This is carry – borrowing money at low rates to finance moves at higher returns.

Now some of this exists in broader investment plans anyway. It is, after all, how a company justifies taking out credit to fund ongoing operational expenses or even expansion. If the cost of servicing the debt is lower than the expected return on what the new money will provide, it makes sense.

However, carry has become an environment onto its own, one in which a return is made for the financial move but nothing of consequence shows up in the economy as a whole.

These days rising yields on 10-year notes (which continue to be the “canary in the coal mine” for those tracking inflationary prospects) are promoting a rising angst that inflation is just around the corner. By my tracking, this is now the fourth time in the last three years talking heads on TV have raised the specter of inflation after reading the rise in the 10-year interest rate.

If they are finally right this time, we can finally say that these guys have “correctly” predicted four of the last one inflation increases.

Even if it does happen this time around, it is not likely to create major market adjustments. It is the financial equivalent of a tempest in a teacup. Rising economic activity, employment, and consumer spending more than counterbalance a rise in prices.

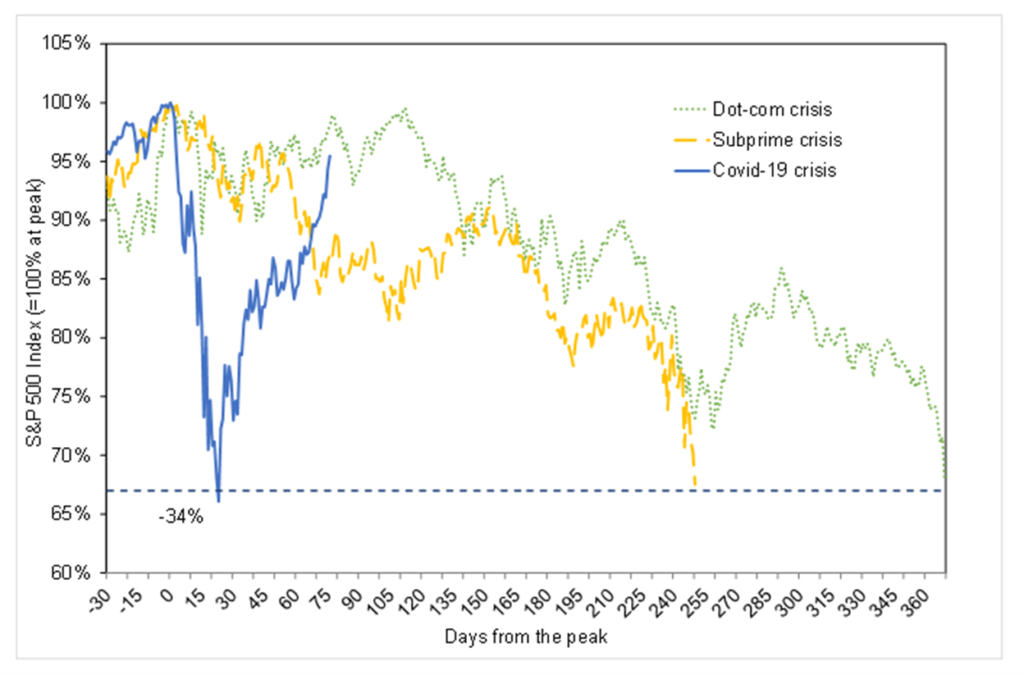

First, the base from which the price increases will arise is hardly a normal market. From February 20 until April 7, 2020, the stock market crashed quicker and deeper than the Dot-com (1995-2001) and the subprime (2008-2009) crises. All three led to recessions, but stocks recovered from the COVID recession much quicker.

Put simply, the crash was the worst…and shortest…in recent US market history. We recovered all of the dive in the S&P 500 by August 5, 2020, less than six months later.

Second, there will be some creative destruction in the aftermath. There are companies which will be unable to maintain activities in the face of rising interest rates. As I have mentioned before, sectors like oil and gas production depend upon lines of credit to fund forward operations rather than proceeds from current sales. These are provided at high risk (i.e., “junk bond”) rates, pegged much higher than investment grade or 10-year yields.

But such liquidations, mergers, and acquisitions have been ongoing cyclically anyway.

Third, should the interest rate situation get out of hand (among other reasons, because of the element I will mention next), the Fed has given indication they are prepared to act. In addition to returning to the market as a purchaser of paper, among its arsenal of tools is the ability to cap yields. Yes, this is rather extreme and the market purists out there will lament that it is an artificial manipulation of fixed income trading.

But let’s get real. The last four administrations (equally of both parties) have intervened. It is hardly a new development.

Finally, a resurgence of trading manipulation in setting debt yields has taken place. Here, the players (led by large investment and merchant banking operations) are making profits off spreads between hyped rates and those reflecting the actual underlying market conditions. It is the fixed income equivalent of shorting stocks.

The profits can be significant. Yields are expressed in basis points (bps), with 100 bps equal to a one percent change in the rate. One private estimate I was provided last week by a contact suggested that the manipulated spreads resulted in a return of almost $1 billion per bps. The 10-year rose 81.5 bps between the start of this year and March 19.

Once again, a market situation has allowed some to profit without actually producing anything.

Yet for those tracking inflation prospects, the most recent reports are reassuring. There is a belief that interest rates will move up this year followed by a reduction toward the end of 2021 and into 2022. But this is largely from figures overlapping historically weak 2020 numbers.

Current consensus forecasts expect gross domestic product (GDP) to remain above trend through the end of 2022. Bank of America, for example, has just increased its forecast for 2021 to 7 percent, higher than the Fed forecast of 6.5 percent.

Meanwhile, the concern over a combination of stimulus payments and economic expansion fueling inflation has abated, at least for now. For February (the last month for which figures are available) core personal consumption expenditures – the Fed’s preferred inflation gauge – rose just 1.5 percent, below the 2 percent Fed target.

There are also indications that demand in some sectors is increasing faster than supply, another signal that any inflationary pressure will be subject to some absorption by normal economic activity.

But with all of this being said, the increase in economic activity now underway can certainly offset any modest rise in inflation that the Fed will allow. Putting workers back on the job and improving the bottom line of businesses is worth it. And if a Fed action now and then can stick it to the manipulators, well so much the better.

This is an installment of Classified Intelligence Brief, your guide to what’s really happening behind the headlines… and how to profit from it. Dr. Kent Moors served the United States for 30 years as one of the most highly decorated intelligence operatives alive today (including THREE Presidential commendations).

After moving through the inner circles of royalty, oligarchs, billionaires, and the uber-rich, he discovered some of the most important secrets regarding finance, geo-politics, and business. As a result, he built one of the most impressive rolodexes in the world. His insights and network of contacts took him from a Vietnam veteran to becoming one of the globe’s most sought after consultants, with clients including six of the largest energy companies and the United States government.

Now, Dr. Moors is sharing his proprietary research every week… knowledge filtered through his decades as an internationally recognized professor and scholar, intelligence operative, business consultant, investor, and geo-political “troubleshooter.” This publication is designed to give you an insider’s view of what is really happening on the geo-political stage.

You can sign up for FREE to Classified Intelligence Brief and begin receiving insights from Dr. Moors and his team immediately.

Just click here – https://classifiedintelligencebrief.com/