Date: 06/06/22

Author: Kent Moors, Ph.D.

As I advised Sigma Trader and PRISM Profits members in our weekly portfolio reviews on Friday, I was in the process of moving around nasty weather coming into South Florida so I could make it out to a meeting of international investors I advise.

Well, the tropical disturbance made the departure difficult but having a client’s private jet to make the trip helped. Any attempt to use airline flights was impossible. All the commercial passenger airports from West Palm Beach down to Miami were closed.

As I write this, it is late evening on Sunday, and we are about to go back into the final session of some highly interesting discussions. There is almost certainty that several billion in investments will be committed to a range of projects before this is done.

Scheduling is always very different with these guys. Meetings began shortly after I arrived with no regard for the almost eight hours I had just spent in the air or the fact that it was a little after 3 AM here. They operate on their own clock (or without regard for one).

This time around, I think it quite likely that I will only be getting some sleep on the return flight.

When this gathering happens (and there has never been one of these highly orchestrated private meetings taking place when money has not been spent at the end), the investments are either private moves, plays on available stock and fixed income paper, or a combination.

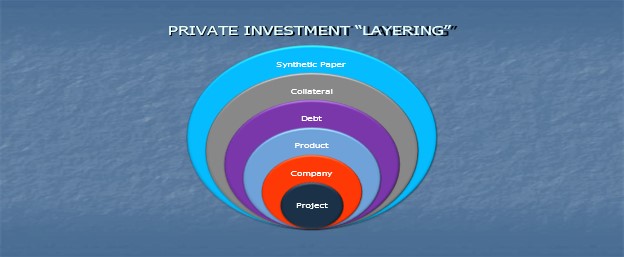

The private approaches usually follow a version of the “layered” multi-faceted approach I first developed for these folks several years ago. This is a process in which moves are made on several fronts at the same time. This is a simplified version:

Equity investments are either collateral to the layering approach or independent.

Early knowledge of the equity moves may well have some benefit for my subscribers. Unfortunately, these usually involve factors that pre-exist the move, making them akin to “insider information.” In these cases, I need to wait until such elements emerge from other sources before I can talk about them or recommend the investment to subs.

That means I cannot talk about what is coming…yet. Suffice it to say that this is going to involve the first step in a significant pivot involving how the big boys deploy cash to offset a rising sector-specific situation. As it happens, it involves energy investment, bringing me back once again to my initial area of specialty.

However, not only can I talk about the environment in which this is going to play out, I already have here in a Classified Intelligence Brief appearing over a year ago.

Read between the lines below and you have an idea of where we are going this time around. The ride coming will be really interesting. This is what I said last May:

There has been a recurring debt constriction cycle facing smaller oil producers in the US which has periodically increased the wave of new bankruptcies and mergers/acquisitions (M&A). Yet the financing picture elsewhere internationally has the potential to generate a more serious kind of result altogether. In the process, it recalls another type of global financing arrangement I knew well.

A few years ago, I would regularly negotiate oil project finance between operating company clients and European banks. At the time, provided the counter parties had successful previous dealings, the approach was rather straightforward despite the unique variegations usually attending one particular deal or another.

Simply sketched out, the entity seeking the funds would conservatively estimate the extractable reserves accompanying the project, the book running bank would lowball the market price, and enough secondary banks would provide a syndicated lowering of the risk.

These types of syndicated loans were easy enough, given the financing market’s need for projects. There were often only three factors that came into play: (1) the lead (or book running) bank would need to have run point on one or more previous money-making projects with the operating company seeking the funding – preferably in the same production basins as the project now under review; (2) syndicating banks would need to be present willing to shoulder risk (thereby reducing the commitment made by the point bank); and (3) the parties would need to agree on an acceptable cost for the funding.

This last aspect was invariably struck on basis points (bps; each “point” representing 1/100 of a percent in interest) added to LIBOR (London Interbank Offered Rate). The higher the “premium” to LIBOR (that is, the higher the bps total), the greater the perceived risk from the overall transaction. LIBOR as the foundation for the syndicated loan also facilitated the relationship among the banks on the lending side, since this was the rate they used among themselves.

The underlying assumption in the entire transaction was the ability to collateralize the value of oil still in the ground. A successful operating company needed prior profitable experience but also the ability to provide partner banks with a recognized ability to underestimate what the company knew it could extract.

Based on the bps total, that deliberate underestimation constituted a known discount rate to the actual value of the operation. This allowed the loan managing bank(s) the ability to estimate their return on money from the leverage provided by the company on the production side.

The risk was also lowered by the main lending institution itself. By factoring in a working price for the oil below expected market rates, the actual return on investment (ROI) would be greater than the revenue amount used to structure the deal.

The approach became untenable for two reasons. First, the credit crunch attending the subprime mortgage crisis in 2009 and the resulting collapse on dollar-denominated asset values worldwide that lingered on the market for several years thereafter made syndication unworkable. Interbank lending dried up. With no other institutions prepared to participate, lead banks had to assume the entire risk. That led to prohibitive financing terms.

The situation was brought home starkly when I was advising a company during finance talks being held in the financial center of London (“The City” was the traditional place to secure such finance). The company was a successful medium sized emerging market oil producer. The lending institution had extensive experience in syndicated loans and had financed two previous profitable projects with the company.

The bank offered three-year, six-month, LIBOR plus 1,295 basis points. That amounted to what was then a prohibitive 14.5 percent annualized interest rate for what the bank admitted was a preferred customer. I told the client we could get a better rate from Tony Soprano.

The second factor is of more recent vintage. The collapse in crude oil prices following the late November 2014 OPEC decision to maintain production and fight for market share undercut the ability for banks to provide realistic below expected revenue estimates as a way of improving profitability on the lending side. When oil prices subsequently recovered several years later and margins could have been entertained to strike new deals, there was insufficient cross-party (lead bank-operating company; lead bank-syndicated party bank) confidence to renew the transactions.

As a result, the global producer-lender relationship required some significant changes. Basic to any doable move remains the gravamen of the previous approach – an ability to collateralize the volume of crude awaiting extraction.

If a new approach could be structured, this remained the best way for the producer to generate finance from the raw material contained at its own drilling locations. Yet banks were looking for ways to contain risk, especially in a volatile pricing environment.

What has emerged is the latest clone in fashioning collateralization.

The rising model requires that producers provide a portion of the in-situ oil as surety for futures contracts. This effectively uses “wet” barrels (actual physical oil available for exchange) not out of the ground to provide value for “paper” barrels (futures contracts on oil consignments) in trade.

Now projects have been hedged for some time as producers use options as a way of insuring price margins moving forward. Using futures contracts in tandem with options has been a time-honored practice to reduce the risk of volatile price changes close to the actual transfer of physical oil. Yet such an approach became difficult as market prices lacked medium to longer-term direction. That has resulted in a troubling development by producers desperate for finance.

It has introduced a third ingredient in the process. The oil being collateralized is not actually in the market. As such, a fiduciary bridge is needed between the paper and wet barrels. The result is becoming a new generation of derivatives.

Intermediary instruments are certainly not new. After all, a futures contact itself is a form of a derivative. However, in this case, the bridge is based upon the finance needed by producers on the one hand and margins required by the banks on the other. The base becomes less the result of any expected actual value of the underlying crude oil.

And that will virtually guarantee volatility as the market price for oil becomes a less reliable indicator. Once the required finance becomes more dependent on the cutting of intermediary paper, the derivatives themselves occupy a progressively more decisive determinant in the overall arrangement. In fact, the pricing is pegged to derivatives of derivatives!

Such securitization routes are reminiscent of very disquieting elements in the MDO (mortgage debt obligation) collapse during the credit squeeze. The derivatives have no value apart from the transaction itself and carry an attendant danger of accelerating credit instability.

This is not sustainable, even when, as currently, crude oil prices are moving up. A decade ago, I devoted most of an entire book to this problem (Kent Moors, The Vega Factor: Oil Volatility and the Next Global Crisis. John Wiley & Sons, 2011).

Two matters subsequently emerge increasing volatility and decreasing accountability.

First, to keep the increasingly artificial securitization sequence going, the price of the asset subject to physical exchange in the market (in this case, oil) becomes dependent upon the need to extract continuing levels of return from paper issued. Such paper becomes increasingly less reflective of the underlying asset’s actual market value. Rather, its “value” becomes dictated by the requirements flowing from external financing requirements. When that no longer can occur, a credit retrenchment ensues.

Over the past six months, roughly since the beginning of 2021, the credit constriction has been accompanied or even preceded by one or more pronounced short plays.

Second, in what follows the pattern of a genuine Ponzi scheme, new and more inventive paper must emerge to provide artificial market value to paper having no intrinsic value on its own.

How bad the results are going to be with the addition of these intermediary dimensions remains unknown because the value conveyed by further waves of paper cannot be independently determined. That uncertainty will further erode confidence in a much broader array of debt paper normally considered secure.

This is the most disturbing aspect and recalls the main liability revealed by the credit squeeze. Contagion migrated to other dollar-denominated asset classes worldwide. Then it was initiated by subprime mortgages. In the new emerging variation, the problem could well become worse.

The overwhelming amount of oil traded on any given day is denominated in dollars, making the new collateralization of an asset having worldwide impact providing a prime conduit for a more destructive expansion of miasma.

Only this time the results may be even more pronounced. If you enjoyed the subprime mortgage implosion, you are really going to like what may be coming in oil. That is because oil has an endemic position in all manner of global economic sectors and more directly undergirds a far broader universe of international tradable assets, both other forms of commodities and more mainstream collateral vehicles.

Dr. Kent Moors

This is an installment of Classified Intelligence Brief, your guide to what’s really happening behind the headlines… and how to profit from it. Dr. Kent Moors served the United States for 30 years as one of the most highly decorated intelligence operatives alive today (including THREE Presidential commendations).

After moving through the inner circles of royalty, oligarchs, billionaires, and the uber-rich, he discovered some of the most important secrets regarding finance, geo-politics, and business. As a result, he built one of the most impressive rolodexes in the world. His insights and network of contacts took him from a Vietnam veteran to becoming one of the globe’s most sought after consultants, with clients including six of the largest energy companies and the United States government.

Now, Dr. Moors is sharing his proprietary research every week…knowledge filtered through his decades as an internationally recognized professor and scholar, intelligence operative, business consultant, investor, and geo-political “troubleshooter.” This publication is designed to give you an insider’s view of what is really happening on the geo-political stage.

You can sign up for FREE to Classified Intelligence Brief and begin receiving insights from Dr. Moors and his team immediately.

Just click here – https://classifiedintelligencebrief.com/